Auto News

Hatchback Cars vs Sedan: Which is Better for Your Lifestyle?

When you look at hatchbacks and sedans, it’s not just about the design. The question is, which one is better for your day-to-day activities. Most people are not searching for the “perfect” car; they just want something that makes every day driving easier. We’ll look deeper into this: hatchback vs. sedan.

What is a hatchback?

A hatchback is a car body style with a back door that swings upward and provides access to the cargo area. The trunk is not separated from the cabin, as in sedans, so that the space inside can be used flexibly. With this, you can carry large items and customize the space to your daily routine.

Main features of a hatchback:

Rear hatch door instead of trunk

The back door opens and provides access to the cargo space. This is useful when you want to load or offload large items that could be more difficult to put through a separate trunk.

Foldable rear seats for additional storage

The interior of the hatchback contains versatile features such as folding, sliding, and stowing. The cargo area contains durable materials, like plastic and fabric. However, the majority of hatchbacks have rear seats that can be folded down, allow you to create more cargo space.

Compact body design

Hatchbacks are smaller than sedans, which is why it is easier to park in tight corners or malls with little parking.

Easy to load large items

The cargo is so close to the cabin that you can carry items as large as sports equipment or grocery bags with no problems. That versatility is a big selling point over traditional sedans and shapes, as well as the principles, for instance, maneuverability and efficiency.

What is a Sedan?

A sedan is a passenger car in a three-box configuration with separate compartments for engine, passenger, and cargo. That gives a more formal three-box car layout than hatchbacks. Sedans offer a balanced combination of comfort and stability.

Main Features of a Sedan

Separated Closed Trunk

The trunk is separate from the cabin, which can protect the luggage from being damaged and ensure it remains safe and can also reduce the noise from the cargo area.

Fixed Rear Windshield

The rear window is fixed as part of the vehicle body, unlike in a hatchback, which means the rear section is solid and strong.

Extended Body Style

Sedans are longer in the wheelbase. It provides better comfort, stability, and flow on the highways.

More Open Passenger Space

The interior has clearly defined seating positions with enough legroom and comfort for everyone on board. Sedans are built for comfort, structure, and road stability.

Hatchback Cars vs. Sedans: The Differences

When you want to compare hatchback cars vs. sedans, you may be overwhelmed by the features. The main difference is how you use the car. There are some people who need flexibility, some who care more about comfort, and some who just want an easy-to-park vehicle. Here are all the key points so you can tell what really matters.

Features

Size

Hatchbacks are compact vehicles that are easier to cross through congested city streets and parking lots. You don’t need to force the car into tight little spaces.

Sedans are longer, however. They need more space when parking, and a U-turn feels a bit heavier. If most of your driving is done around town, a hatchback will just make life easier.

Maneuverability

Hatchbacks give you a light, quick feel on the road. Changing lanes, making sharp turns, or squeezing into a tight spot on the right is no problem. There is nothing wrong with sedans’ handling; they just need a bit more effort.

Cargo and Storage

Hatchbacks make carrying things easy. They have big lift gates that swing up, so you get lots of vertical space. If you need more room, just fold down the back seats.

Sedans work differently. Their trunks are separate, so they’re more private and quieter. But you don’t get much height or a big opening, which means fitting larger items can be quite difficult.

Ride Comfort

Sedans feel better on long drives. They give you a smoother ride, thanks to things like their separate trunk and suspension that’s built for comfort. Hatchbacks, on the other hand, are easier to handle around town.

You get better access to your cargo, and extra headroom, so they’re more flexible for city life even though you may notice more road noise.

Fuel Efficiency

Hatchbacks and sedans both do well when it comes to fuel efficiency, but the real differences come down to the specific model and not the type of car. In most cases, hatchbacks handle city driving a little better because they’re smaller and lighter, so they use less gas in traffic.

Sedans get a slight edge on the highway because of their aerodynamic shape. Still, the gap isn’t huge, and it depends on which car you’re looking at.

Style and Design

Sedans stick to the classic “three-box” shape, so you get a separate trunk and that traditional, polished look. Back passengers usually have more legroom, too. But hatchbacks go with a “two-box” design and a rear lift gate.

They’re a lot more versatile when it comes to cargo, easier to park in tight city spaces, and look a bit sportier and more modern.

Road Presence

Sedans stand out more because of their length and formal design. Hatchbacks feel a bit more agile and are built for city life. They’re compact, easy to maneuver, and have a more urban, modern style. Sedans, though, have a longer wheelbase and a lower stance, giving off that timeless, sophisticated feel.

Flexibility

Hatchbacks are great if you need space; they’ve lift gates and folding back seats. You can pull bigger or odd-shaped material without much trouble. Sedans really focus on comfort and classic style. Their separate trunks keep your belongings out of sight and make the ride a bit quieter.

If you live in the city, hatchbacks fit in better and handle tight spots well. Sedans come off as more polished and refined.

Ease of Use

Hatchbacks just make life simpler; you can squeeze them into tight parking spots, throw loads in the back through a big rear hatch, and deal with difficult cargo without much trouble. Sedans give you more privacy in the back and a smoother, more polished ride.

When you’re stuck in city traffic, hatchbacks feel quicker and easier to handle. Sedans hold the road better when you’re picking up speed. _

Compact Movement

Compact hatchbacks focus on practicality and are easy to handle in city traffic. They have a rear lift gate that gives you quick access to the cargo area, and folding down the seats means you get more space when you need it.

Sedans put comfort and security first. The separate trunk keeps your belongings out of sight, gives passengers more privacy in the back seat, and usually blocks out road noise better than a hatchback.

Comfort

Sedans make long drives more comfortable. You get more space to stretch your legs in the back, the ride feels smoother, and things stay quieter inside. On the flip side, hatchbacks are all about utility.

There’s extra headroom, it’s easy to load things in the back due to the lift gate. Both types handle passengers just fine.

Structure

Hatchbacks have a “two-box” design, which means the engine sits in front and the passenger and cargo areas share the same space. You open the back with a lift gate that swings up.

Sedans are a bit different; they split the car into three areas: engine up front, people in the middle, and a trunk in the back.

Hatchbacks give you more flexibility, especially when you need to load bulky things; also, you get more room for taller items. Sedans keep your belongings tucked away in a separate trunk and typically give you a quieter, smoother ride.

Drivability

Hatchbacks are great if you’re driving through the city; they’re smaller and lighter, so you can squeeze into tight parking spots and handle busy streets without much stress. Sedans feel steadier and quieter when you’re cruising at higher speeds because of their longer wheelbase and the separate trunk.

If you need to carry different kinds of cargo, hatchbacks make that pretty easy. But when it comes to sitting in the back seat, sedans have more room and comfort.

Pros of Hatchbatch

- Flexible Cargo Space

This is the biggest advantage. Without a separate trunk, you can fold the back seats down to create a broad, usable area. It allows you to transport larger items far more easily than a sedan.

- Easier to Drive in Tight Areas

Hatchbacks are normally small, which is suitable when it comes to parking and maneuvering through traffic. You don’t need as much room to turn or squeeze to park your car.

- Better Fuel Efficiency

Because they’re lighter, hatchbacks have better gas mileage. It is the small difference that makes all the difference when you drive every day.

Cons of Hatchbacks

- Less rear seat space

Most hatchbacks are small, so the legroom in the backseat can feel overcrowded, especially if you’re tall.

- More Cabin Noise

As the boot is not a separate space, external noise can infiltrate more readily inside.

- Limited Privacy for Luggage

There’s no lockable trunk, so belongings in the back are more exposed unless you put a cover on them.

- Not Stable at High Speeds

Hatchbacks feel lighter on highways, especially when driving fast compared to sedans.

- Less formal appearance

They are practical, but they don’t always have the same ‘executive’ look that people expect from a sedan.

Examples of Hatchback Cars

Here are some popular hatchback models:

- Honda Civic Hatchback

- Toyota Corolla Hatchback

- Volkswagen Golf

- Ford Focus Hatchback

- Hyundai i30

- Kia Rio Hatchback

- Peugeot 208

- Mazda3 Hatchback

Sedan Pros and Cons

Pros of Sedans

Better Ride Comfort

Sedans are built with a longer wheelbase, which helps smooth out bumps and rough roads. The drive feels more stable, especially at higher speeds.

Quieter Cabin

The separate trunk design helps reduce road noise. You may notice this when on a long trip.

Balanced Handling

Weight distribution in sedans is usually more even, giving better control on highways and during turns.

More Refined Appearance

Sedans have a clean, structured look. It gives that more formal and presentable look.

Secure Trunk Space

Since the trunk is separate, it hides your luggage and also protects them instead of an open cargo area.

Cons of Sedans

Limited Cargo Flexibility

The fixed trunk space means you can’t easily carry large or oversized items.

Less practical for mixed use

If you regularly carry different types of loads, the sedan design can feel restrictive.

Longer Body Size

Parking and maneuvering in tight spaces can take more effort unlike smaller cars.

Lower Ground Clearance (in many models)

Some sedans struggle on rough or uneven roads than larger vehicles like an SUV.

Related Post:FWD vs AWD: Which Drivetrain is Actually Better for You?

Examples

Here are some popular sedans across different categories:

- Honda Civic

- Toyota Corolla

- Honda Accord

- Toyota Camry

- Hyundai Elantra

- Nissan Altima

- Mercedes-Benz C-Class

- BMW 3 Series

- Kia K5

- Volkswagen Passat

FAQs

- What is a hatchback?

A hatchback is a car with a rear door that opens upward, giving easy access to the cargo area. The seats often fold down for extra space when needed.

- How is a sedan different from a hatchback?

Sedans have a separate trunk and a longer body. It gives a smoother ride. On the other hand, Hatchbacks are more flexible. They’re perfect for city driving.

- Are hatchbacks good for long trips?

Yes, they can handle long drives, but sedans usually offer a quieter and more comfortable ride.

- Should I choose an SUV or a hatchback?

SUVs are great for space, off-roading, or family trips. Hatchbacks are better for city driving, easy parking, and fuel efficiency.

- Do hatchbacks save on fuel?

Most hatchbacks are lighter than sedans or SUVs, which usually means they consume less fuel in daily driving.

Conclusion

Hatchbacks are small, flexible, and easy to park. For sedans, they’re built for comfort, especially on longer drives where you just want to sit back and relax.

Sedans have that tough, dependable vibe, and they fit just about everything without making you sweat over space. Honestly, what matters most is how the car fits into your everyday life.

Want more car tips and updates? Subscribe now and be part of the conversation.

The comparison between the Honda Civic and Toyota Corolla didn’t start today. These are different brands, but intending buyers always like to compare them. Both cars have improved features. But owning a car is not all about features. You need to know how they work.

On major roads, you may notice that there are many Hondas and Toyota Corollas. You know why? The reliability and maintenance costs are low. Should any damage happen to the car, they are available in several auto shops, and all these count.

About the Honda Civic Car

The Honda Civic Sedan and Hatchback rank as the top choices among buyers. Both models have similar powertrain selections.

Honda Civic Models (2020–2025)

Honda Civic Sedan Models

These are the most common Civic models.

- LX (base model)

- Sport

- EX in 2020–2021

- EX-L (some markets or years)

- Touring / Sport Touring (Hybrid in 2025).

In the sedan lineup, they have:

- LX

- Sport

- Sport Hybrid

- Sport Touring Hybrid

Honda Civic Hatchback Models

These have a sportier design.

- LX (previous years)

- Sport

- EX / EX-L (previous years)

- Sport Touring

In recent models (2022–2025), hatchbacks focus more on:

- Sport

- Sport Touring (including hybrid versions)

Honda Civic Coupe (Discontinued)

Available up to 2020

- LX Coupe

- Sport Coupe

- EX Coupe

- Touring Coupe

Note that Honda stopped producing the coupe after 2020.

Honda Civic Si (Performance Trim)

Civic Si Sedan (manual transmission only)

Honda Civic Type R (High Performance)

This is the top-tier performance model.

Civic Type R (Hatchback only)

Honda Civic Hybrid (Reintroduced in 2025)

Models:

- Civic Sport Hybrid

- Civic Sport Touring Hybrid

Civic models from 2020–2025, fall into:

- Sedan (4-door)

- Hatchback (5-door)

- Coupe (2-door; discontinued after 2020)

- Performance models (Si & Type R).

About Toyota Corolla

The Corolla has its own style. It’s always been about being reliable. Newer models run more smoothly, make less noise, and are fuel-efficient compared to older versions, particularly the hybrid ones.

Eleventh Generation (2012–2019)

This generation comes as sedans and wagons.

Twelfth Generation (2018–Present)

Introduced around 2018, this generation expanded the Corolla lineup to include:

- Sedan

- Hatchback

- Estate / Touring Sports (in some markets)

- GR Corolla (high-performance hatch).

Toyota Corolla Trims and Models

Standard Corolla Trims

- Toyota Corolla L: Basic entry-level model

- Toyota Corolla LE: Most common comfortable daily driver

- Toyota Corolla SE: Sportier styling and suspension

- Toyota Corolla XSE: Premium, more features and technology.

Hybrid Versions

- Toyota Corolla Hybrid LE: Base hybrid focused on efficiency

- Toyota Corolla Hybrid SE: Sportier hybrid feel

- Toyota Corolla Hybrid XLE: Premium hybrid with extra features

- Trim names like L, LE, SE, and XSE are used in the U.S., Canada, and some foreign markets.

- Other regions may have different badges, such as GLi, XLi, or Altis.

Honda Civic Features (2020–2025)

Between 2020 and 2025, the Honda Civic transformed from a basic compact car to something more refined. The features include:

Engine and Hybrid Powertrain

The Civic models from 2020 to 2025 have a standard 2.0L 4-cylinder engine. In addition, newer versions include a hybrid system that combines a gasoline engine with electric motors, and delivers up to 200 horsepower. The base engine provides reliable power for daily driving.

On the other hand, the hybrid setup has stronger acceleration and it doesn’t consume much fuel.

Continuously Variable Transmission (CVT)

Since 2020, the Civic has been using a CVT instead of the usual automatic transmission. This system doesn’t shift gears in the traditional sense. It adjusts constantly.

Interior Design and Cabin Layout

Between 2022 and 2025, it featured a streamlined dashboard design with mesh panels that covered the air vents, a higher interior material in all trims. The simplified layout keeps your eyes steady and focused on the road.

Controls are placed where hands naturally reach, reducing the need to look away while driving.

Infotainment System and Connectivity

Modern Civic models come with touchscreen displays. Most are 7-inch to an optional 9-inch version. They include smartphone integration and, in the higher trims, digital instrument clusters. These features are all about convenience.

You can connect your phone and access navigation, music, and calls without separate you needing devices. And the system responds quickly. The Civic keeps things smooth and responsive.

Honda Sensing Safety Suite

Honda has made its safety system standard on most Civic trims. Adaptive cruise control, lane-keeping assist, and automatic emergency braking are included.

These features actively support the driver. One is an adaptive cruise control that keeps a set distance from the vehicle in front, and hills can be easier on passengers on long trips.

Lane-keeping assist also keeps the car centered, particularly on highways. If it senses an impending impact, emergency braking takes over. The aim is not to take over driving but to reduce errors and ease stress behind the wheel.

Suspension and Handling System

A big part of the Civics’ identity is its suspension tuning. Honda understands that balance was the answer. With this feature, the car doesn’t over-bounce on rough roads, and it doesn’t feel loose when you turn. That makes it easier to drive particularly at high speed or on bumpy roads.

Space

The Civic seats five people comfortably. Its back seats are spacious, and the trunk is wide. Also, the hatchback model adds versatility, which means drivers can carry larger items when necessary.

Related Post:Why You Should Never Ignore Wheel Bearing Noise

Toyota Corolla Features (2012–2025)

Engine and Powertrain

In 2012, the Corolla came with a 1.8L engine that had four cylinders and delivered about 132 horsepower. Drivers could choose between a manual and an automatic transmission. Fast forward to 2025, and it featured a more robust 2.0L engine producing up to 169 horsepower.

Essentially, the Corolla provides steady and reliable power. The newer engines offer slight improvements in efficiency and responsiveness.

Hybrid System

Toyota added hybrids to the Corolla lineup, and by 2025, they became a big selling point. These systems blend gasoline engines with electric motors to boost fuel efficiency. On the road, this hybrid setup cuts down fuel usage a lot, especially in traffic.

Moreover, it runs quietly and smoothly. Drivers can switch between electric and gas power automatically.

Transmission System (Manual, Automatic, CVT Evolution)

In 2012, the Corolla included a 4-speed automatic and a 5-speed manual transmission. But as time went by, Toyota switched to CVT systems. This shift increased fuel efficiency.

By the year 2025, most trims had CVTs as standard equipment. The Corolla’s CVT, much like that of the Civic, removes gear shifts, keep rides smooth. Also, it lowers fuel use.

Interior Comfort and Layout

The Corolla’s interior has always made sense. Back in 2012, it had enough space, easy controls, and room for passengers. In 2025, they improved on the interior.

Infotainment and Connectivity

Older models of the Corolla had basic audio system, such as Bluetooth and USB connectivity. Today’s models have bigger touchscreens, smartphone connectivity, and enhanced software systems. The features make connection easy.

Toyota Safety Sense

The safety suites are available on newer Toyota Corolla models. They include lane departure warning, adaptive cruise control, and pre-collision systems, among other things.

These tools are similar to that of Honda’s lineup. However, there is a key difference: Toyota’s approach leans towards caution. Their system opts for stable and predictable actions over quick responsiveness.

Practical Space and Everyday Use

Like the Civic, the Corolla has a five-seater and a usable trunk (roughly 12 to 13 cubic feet, but it depends on the model year).

This asset covers daily life, transportation, shopping, and traveling. Not the biggest in its class, but definitely the most consistent. The back seats also split-fold.

Honda Civic vs Toyota Corolla: The Comparison

Driving Feel

The Honda Civic is more responsive and easy to control. The steering has some weight to it, and the car responds immediately when you turn the wheel.

Engine Performance

The Civic picks up speed faster, especially in its turbo and hybrid versions. It feels more responsive when you need to merge into traffic or pass another car. On the other hand, the Corolla provides a consistent power flow.

It’s not sluggish, but not as responsive as that of the Honda Civic. The Civic delivers performance on demand, while the Corolla offers steady reliability.

Fuel Economy

Corolla (both gas and especially the hybrid) is more fuel efficient. It conserves fuel better regardless of how you drive. The Civic hybrid is efficient too, but it combines power and economy. Corolla wins if you want to save money on fuel. However, if you want performance over fuel efficiency, the Civic is better.

Interior Quality

Civic has a better interior. Its materials are higher-quality, the layout is neater, and it looks modern inside and out. But the Corolla may not feel luxurious, but it’s easy to use, and it’s comfortable, too.

Technology and Infotainment

The Civic offers a more refined experience, with a fast-responding, high-quality display. The Corolla, however, leans more towards simplicity and reliability. Its design might not impress, but it consistently handles tasks well.

While the Civic provides a modern feel, the Corolla cares about performance and reliability. Do you need heavy technology or just something simple like radio, USB, Reverse camera, etc.? This will help you to make your choice.

Reliability

Both cars are solid choices, but the Corolla stands out for its long-term reliability. You don’t have to worry much about wear and tear of parts. Their parts hardly fail. As for Civic, it is reliable but it requires more regular maintenance than the Corolla.

Maintenance Cost

The Corolla has a cheaper maintenance cost. In addition, people go for Toyota because the parts are easy to find, and the service is less expensive, too. The civic parts are also available in aftermarkets, but the prices are high compared to the Honda Civic.

Resale Value

Both cars maintain their value well, though the Corolla often has a slight advantage. Buyers have confidence in its reliability, so demands are high. While the Civic sells easily, too, more buyers usually prefer the Corolla when shopping for a used car. So, it attracts more interest when you put it up for sale.

FAQs

- Which is better: the Honda Civic or the Toyota Corolla?

There isn’t a single “better” option here, and that’s why the Honda Civic vs Toyota Corolla debate keeps going. The Civic is better if you care about driving feel, design, and a more refined experience.

The Corolla is better if you want reliability, lower costs, and resale value. But it depends on your priorities, not the car itself.

- Which car lasts longer, Civic or Corolla?

Both cars can last a long time, but the Corolla is known to last longer especially if proper maintenance is followed.

- Is the Honda Civic worth the extra cost?

The Civic delivers a better driving experience, a more sophisticated interior, and a more modern technology. If those things matter to you daily, the extra expense is worth it. If all you want is a reliable car to get you from point A to point B, the Corolla is far better.

- Which has better fuel economy, the Civic or Corolla?

The Corolla, especially the hybrid version, is typically better for fuel economy. It’s designed to maximize efficiency without requiring any effort from the driver. The Civic hybrid is also efficient, but it balances fuel savings with performance. If your main goal is spending less on fuel, go for the Toyota Corolla.

- Which car is better for daily commuting?

Both work well, but in different ways. The Corolla makes commuting easier because it’s smooth, predictable, and comfortable over long periods. The Civic makes commuting more enjoyable because it feels more responsive and engaging. For long drives, Corolla reduces stress. If you want to enjoy the drive a bit more, the Civic stands out.

Wrapping Up

The Honda vs. Toyota debate doesn’t seem like something that’ll end soon. Although they are different car brands, the two are popular because of their fuel efficiency, available parts, resale value, and affordable maintenance costs.

If you need a car for personal use and want a sporty feel, I recommend a Honda Civic. The Toyota Corolla can withstand everyday driving and can be used for ride sharing. The look is not among the best, but surely one of the most dependable cars.

Still have questions? Drop them in the comment section, and kindly like us on all our social media pages.

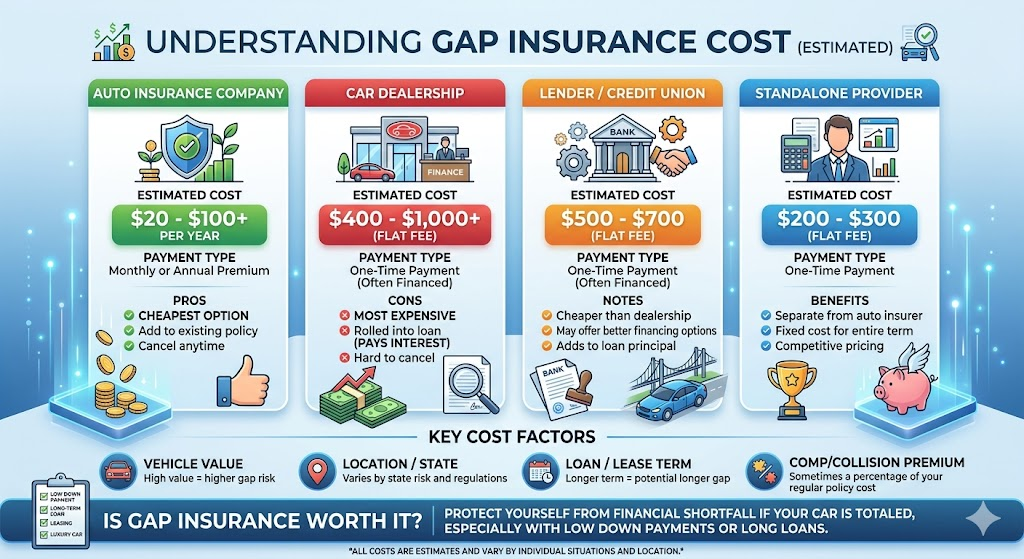

Toyota Financial Services, Ford Credit, and Honda Financial Services, allow refinancing and gap insurance. While filling out a form, the dealership may ask if you want Guaranteed Auto Protection (GAP coverage). Don’t be quick to say yes or no if you have no idea what they are talking about. Find out how much gap insurance costs and whether you even need it.

Most buyers at this point hurriedly tick the box without knowing what they just signed up for. Once you agree to the terms and conditions of the coverage, you must keep to the agreement. And some terms you may come across is Guaranteed Auto Protection or Coverage.

What Is Guaranteed Auto Protection (Gap Coverage)

Before we get to the cost, let’s clarify one basic question: What is gap coverage, and why does it keep appearing whenever someone talks about car financing?

In essence, gap insurance covers you for the shortfall between what your standard car insurance pays out after a total loss and what you still need to pay on your loan or lease. It is applied only when the car is declared a total loss or stolen and not found.

Here’s where it gets interesting. Cars apparently don’t retain value the way people think. Once you drive a new car off the lot, its resale value begins to drop. Your loan, however, doesn’t reduce.

You’re still paying interest on the full amount you borrowed. So it’s quite easy to owe more on your car than it is actually worth just a month or two after you buy it. That’s not poor financial planning, but how depreciation works.

“Gap insurance covers the difference between your car’s value and the amount you still owe on your loan. When drivers hear stories of people paying for a car that has already been totaled, they start asking, “How much does gap insurance cost?”

When gap coverage is included in your car insurance policy, most drivers are hit with a fee of $20 to $40 per year at most, which converts to about $2 to $5 per month. It is one of the cheapest add-ons that you can attach to a car insurance policy.

Buying gap insurance from a dealer can cost more. They charge a one-time fee ($400-$800+) added to your loan, rather than a small monthly payment. So, you are paying a premium price for the exact same coverage.

Gap insurance usually costs between $2 and $14 per month, or $24 to $168 annually. Rates depend on your vehicle’s value, loan amount, and state.

How Much Is Gap Insurance per Month with Major Insurers

Gap coverage is calculated differently by insurers. One company might refer to it as “gap insurance,” while another uses the term “loan/lease payoff coverage.” They have the same purpose, but the amount and definition of coverage are different.

Take, for example, Geico, which provides gap coverage in some states and not as part of a comprehensive policy. Progressive has a similar product called loan/lease payoff coverage, but with important distinctions: it rarely covers the entire amount; often covering only the gap up to 25% of the car’s actual cash value. (research yours for the exact percentage).

These coverage thresholds can make a huge difference in your payout when you make a claim.

Your gap insurance premium is calculated with these considerations in mind:

- Vehicle Value: Higher-end vehicles have a greater potential “gap” between their value and loan balance, driving up costs slightly.

- Loan Terms and Amount: The more you financed the car’s cost or the longer your repayment term, the greater the chance you’ll owe more than the car’s worth and the higher your cost.

- Location: Residing in high accident or theft areas may raise your premium.

- Driving History: Although gap insurance is associated with your loan, the car insurers may consider your driving history when determining how much your overall policy will cost. A clean record keeps costs down; a claims history can increase them.

Gap Insurance Cost Through a Dealership vs. an Insurance Company

It’s one of the largest areas where drivers overpay and don’t even know it. You’re already concentrating on interest rates, monthly payments, and the paperwork, so when the dealership presents gap protection, it seems like just another box to check before you drive off in your new car.

Gap insurance is typically offered at dealerships as a one-time fee ($400–$800), which is then added to your auto loan, so you end up paying interest on it for the duration of the loan. This brings the accessory rate much higher than the sticker price.

Or you can buy gap insurance from your car insurance provider for a small additional premium. You get the same basic coverage, but you don’t pay the interest.

The difference in prices can pile up. “It’s cheaper to pay a couple of dollars a month than to pay a few hundred all at once.”

Why Gap Insurance Exists Primarily on New Cars

Most cars lose about 15 to 20% of their value within the first year, sometimes even more, depending on the make and model. That means that a vehicle you paid $30,000 for could realistically be only worth $24,000 or $25,000 by the time you’ve made just under a year of payments.

Nothing is wrong with the car. The car value is only depreciating, that’s all.

When you buy a car using financing, you are repaying the entire cost including the interest. At the initial stage, most of your payment is going toward interest instead of principal. So your vehicle is depreciating fast, but your loan balance is decreasing slowly.

New cars depreciate quickly and often cause a major gap between the value of the car and the loan balance for a long time. Used cars, on the other hand, have already taken that steep initial depreciation hit, so the loan-to-value gap is much smaller.

Do I Need Gap Insurance?

You likely need gap insurance if:

- You financed most of the car.

- Your loan term is longer than 60 months.

- You rolled old debt into a new car loan.

- You made a small down payment.

- You may not need it if:

- You paid cash.

- Your loan balance is already lower than the car’s value.

- You made a large down payment.

So the answer to “do I need gap insurance depends on several factors like the above.

How State Laws Affect Gap Insurance Cost

Gap insurance is not mandatory; some leasing companies and lenders may require you to add this coverage to your finance contract if you are not able to show proof of insurability.

Rates for insurance also vary by region. Those driving in areas that see a lot of claims often pay more, as total-loss claims are more frequent.

So your monthly cost in Texas or California, for instance, could vary even if you had the same car model.

What Gap Insurance Does Not Cover

Gap coverage is extremely particular. It simply covers the difference between the amount you owe on your loan and the actual value of your car in the event of a total loss.

It does not cover:

- Engine failure

- Repairs

- Missed loan payments

- Late fees

- New vehicle replacement

Gap Insurance vs. Loan or Lease Payoff Coverage: Are They the Same?

A few insurers, like Progressive, don’t call it “gap insurance.” They refer to it as loan or lease payoff coverage. It sounds different, but it essentially does the same thing: If your vehicle is destroyed or stolen, it pays the gap.

There is a limit, though. It’s usually about 25 per cent over what the car is worth. That’s fine for most people, but if you owe way more than your car is worth, it won’t cover even half your liability. It’s not exactly the same as gap insurance, but it is comparable.

For instance, if your loan was high and your down payment was low, you could still owe a balance even with this coverage.

When Gap Insurance Stops Being Useful

Gap insurance is not forever.

There’s no longer a gap to insure once your loan balance is less than the market value of your car. Gap insurance is only relevant while your vehicle loan balance is less than the market value of the car. It’s simple to get gap insurance when you buy a car, but many drivers fail to cancel it afterwards.

Months or years later, they don’t know they are still paying for the coverage they no longer need.

Call your insurer to end the monthly fee. It’s a little bit of savings, but with time, it all adds up. And it’s just nice to know that you aren’t paying for something you don’t need to. Gap insurance only provides value during the first few years of a loan or lease; beyond that, it’s extra, and it’s safe to cancel it.

Related Post:Dashboard Indicator Lights Meanings Explained

Factors That Change Gap Insurance Cost

Insurers look at risk and loan structure.

Key factors include:

- Loan-to-value ratio

- Vehicle depreciation rate

- Loan length in months

- Whether the car is leased or financed.

Luxury vehicles and fast-depreciating cars often come with slightly higher premiums.

Why Some People Think Gap Insurance Is a Scam

There are many drivers who will tell you gap insurance is a waste of money. For instance people that:

- Never had a total loss

- Paid off their loan early

- Or had enough equity to start with.

For example:

Car value: $20,000

Loan balance: $25,000

Accident total loss payout: $20,000

If you don’t have gap insurance coverage, you’ll owe $5,000 out of pocket.

The policy covers that gap, and then pays off the loan.

Should You Buy Gap Insurance From the Dealer or Your Insurance Company?

Dealers get commission on the add-ons. Gap coverage is priced by the insurance company as a policy add-on.

So dealership gap insurance is usually several times more expensive for comparable coverage. This is one of the simplest methods by which buyers overpay when financing a car.

When you’re shopping around, always check your insurer first.

How Gap Insurance Works With Used Cars

Most people think gap insurance is for a new car and not a used one, and this is not true. When you have a new car, depreciation hits the hardest right in the first couple of years, so gap coverage is typically most beneficial during that early ownership window.

With a used car, a large part of that value drop has already taken place by the time you buy it. This means that the amount of the loan and the market value of the car are closer in value, so the “gap” is smaller to begin with.

However, there are scenarios where it is worth it to get gap coverage on a used car. Even with used vehicles, you can still owe more than its worth if you financed close to the full price, took a long loan term, or rolled over negative equity from a previous car.

Gap coverage is the one type of insurance that can prevent you from owing money for a vehicle you no longer own.

The timing, however, is what’s different. Used cars reduce the gap quickly as you pay and the value of the car holds firm. So while gap insurance will still help you, you may only need it for a shorter period compared to someone who just drove a brand-new car off the lot.

How Long Should You Keep Gap Insurance?

Most financial advisors suggest that you keep gap insurance until:

- Your loan balance drops below market value.

- Or you refinance to shorter terms.

And that’s because most drivers hit this between the 18- and 36-month mark of their loan term. For the most part, it is safe to remove them after that.

Average Gap Insurance Cost Compared to Other Car Expenses

Typical costs are:

Expense Monthly Cost

- Fuel: $120–$250

- Insurance $80–$180

- Car payment: $300–$600

- Gap insurance: $2–$14.

Final Thoughts: Is Gap Insurance Worth the Cost?

Car insurance is a minor add-on, but it’s essential since it covers the difference between loan payments and the depreciation of the car. “Once your car is totaled, you are exposed to huge financial risk since the value of the car is depreciating faster than you’re paying off the loan.

GAP insurance is an asset if you have a big loan, lease your car, or own one that depreciates rapidly. But if you bought it outright, or you owe less than what the car is worth, you don’t need it; that will be an unnecessary expenditure.

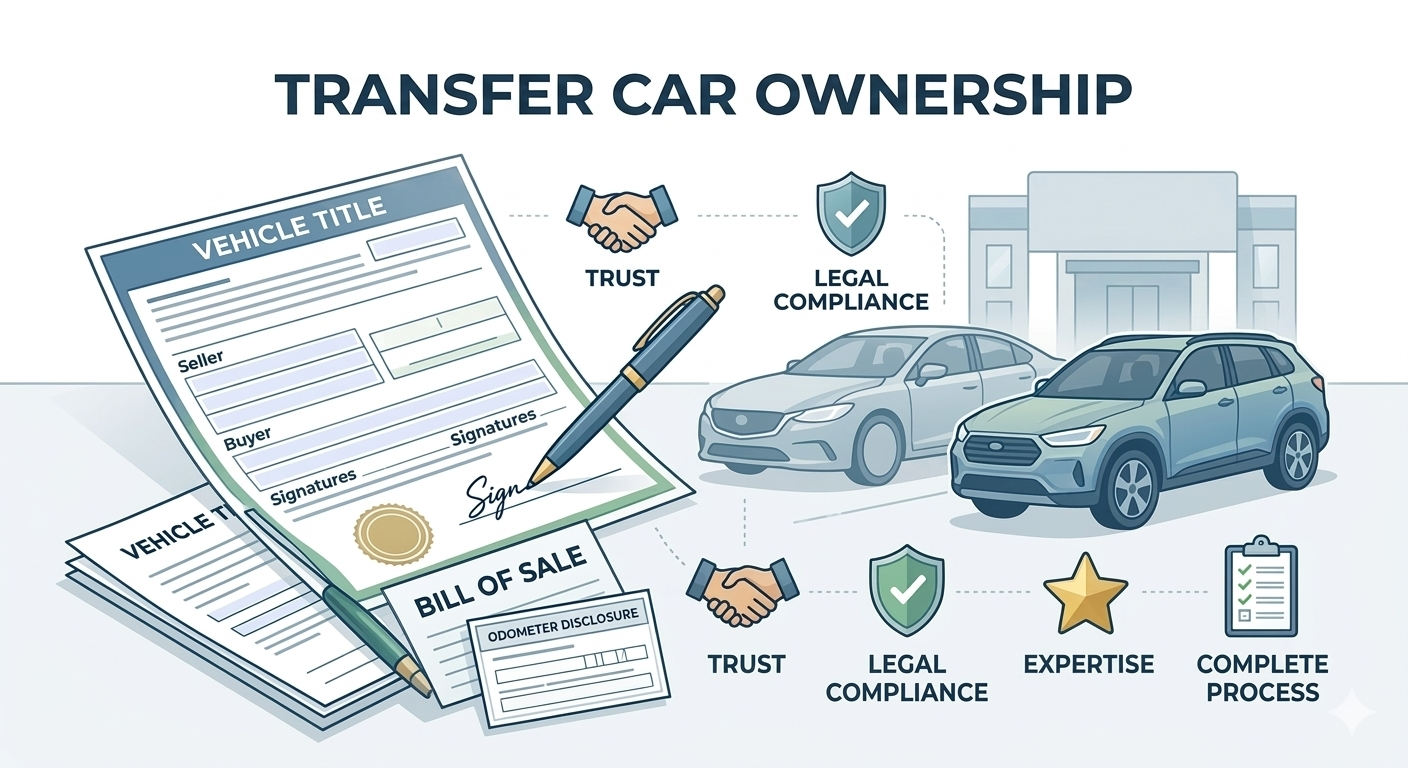

Transfer Car Ownership:There is more to transferring car ownership than simply giving the keys. It is a legal shift in accountability from a regulatory standpoint. If handled improperly, the buyer may have trouble registering the car or obtaining insurance, and the seller may continue to be responsible for any traffic infractions or collisions involving the vehicle.

This procedure needs to be viewed from the perspectives of financial security and legal compliance.

Getting Ready: Compiling the Crucial Records

Both parties need to have their paperwork ready before the handshake. The fundamental documents are the same everywhere, but regional requirements differ slightly.

- The most important document is the vehicle title (also known as the “Pink Slip”). It demonstrates legitimate ownership. The buyer must receive a signed copy of the title from the seller. Before the transfer can take place, any lienholders (such as banks) must be satisfied and cleared.

- The bill of sale serves as an official receipt. The purchase price, the date of sale, the VIN (Vehicle Identification Number), and both parties’ names and signatures should all be included.

- Odometer Disclosure Statement: In order to prevent fraud, local and federal laws frequently mandate that the mileage be accurately recorded at the time of sale.

- Maintenance Records: Providing a service history enhances “Trustworthiness” and can support a higher asking price, even though it is not legally necessary for the transfer.

The Seller’s Obligations: Safeguarding Your Liability

Your main objective as a seller is to cut off any legal ties to the car as soon as it leaves your driveway.

Notice of Release and Transfer of Liability

A “Notice of Transfer” or “Release of Liability” must be submitted to your local transport authority or Department of Motor Vehicles (DMV) in many jurisdictions. This lets the government know that you are no longer liable for any future tickets, registration costs, or illegal use of the car.

Insurance Termination

Until the buyer has physically taken possession and the title is signed, do not cancel your insurance. But to avoid paying premiums on a car you no longer own, let your agent know as soon as the deal is finalised.

Eliminating Plates and Personal Property

Remove all personal belongings and electronic information (such as synced phone contacts or saved GPS home addresses). In many states and nations, the seller retains the licence plates rather than the vehicle. To find out if you should keep your plates or give them to the buyer, check your local laws.

Obtaining Legal Title: The Buyer’s Duties

The goal of the transfer procedure for the buyer is to demonstrate that the car is now theirs and that it is legal to drive.

The Emissions Test and Inspection

Make sure the car passes any required safety or emissions inspections before completing the transfer. A “Roadworthy Certificate” or “Smog Check” may be required in some areas before a title transfer can take place.

The DMV Consultation

You usually have a window of time (usually 10 to 30 days) to visit the DMV after you have the signed title and bill of sale. You’ll have to:

- Send in the title that has been signed.

- On the purchase price, pay sales tax.

- Pay the title and registration fees.

- Show evidence of your current insurance.

Dealing with Unusual Conditions

Not all transfers are simple sales. Unique situations are subject to different rules:

Giving a Car as a Present

You might not have to pay sales tax when giving a car as a gift to a family member. To appease tax authorities, a title transfer and probably a “Affidavit of Gift” must still be completed.

Inheritance

Unless the car was held in a trust or has a designated “Transfer on Death” (TOD) beneficiary, the transfer typically requires a death certificate and “Letters of Administration” from a probate court if the owner has passed away.

Purchasing a Lease

When the buyout price is paid, the leasing company—the real owner—will send you the title if you are buying out your own lease. In order to re-register the vehicle in your name alone, you must then bring that title to the DMV.

Preventing Fraud and Typical Mistakes

Be mindful of these warning signs in order to preserve the “Trustworthiness” component of the transfer:

- Title Washing: Watch out for titles that have been “cleared” of flood-damage or salvage notations by transferring the vehicle between states. Always use services like AutoCheck or Carfax to run a VIN check.

- Curbstoning: To get around lemon laws, a professional dealer may pretend to be a private seller. Proceed with extreme caution if the seller’s ID and the name on the title don’t match.

- Unsigned Titles: Never purchase a vehicle from a vendor who says they will “send the title later.” The payment and the title transfer ought to occur simultaneously.

Related Post:How to sell a car with a loan: The Stress-Free Guide

The Financial Infrastructure: Managing Funds Securely

The most dangerous part of any car ownership transfer is the moment of payment. Both parties must use safe techniques that leave a paper trail in order to maintain high trustworthiness.

The Danger of Digital vs. Cash Payments

Although “cash is king” in private sales, there is a physical risk involved. Meeting at a bank is frequently safer for transactions exceeding $5,000.

- The best option for private sales is a cashier’s cheque. The buyer guarantees the funds by obtaining a cheque from their bank. Expert Advice: To prevent sophisticated counterfeit scams, the seller should go with the buyer to the bank to observe the cheque being printed.

- Escrow Services: Using an online escrow service serves as an impartial third party for long-distance or expensive classic car sales. Until the buyer attests to receiving the car and a legitimate title, they retain the money.

- Digital transfers: While apps like Venmo and Zelle are handy, they frequently have daily limits and provide little to no recourse in the event that a transaction goes wrong. Make sure the recipient is who they say they are before clicking “send.”

Comprehending Sales Tax and Appraisal

In an attempt to “save money,” buyers frequently request that the seller write a lower purchase price on the Bill of Sale. Steer clear of this. “Fair Market Value” databases, such as the Kelley Blue Book or NADA, are used by tax authorities. The DMV may flag the transaction, audit the buyer, and impose taxes based on the higher value even if the reported price is much less than the market average. Additionally, this keeps the seller from participating in tax fraud.

Technical Verification: Title Brands and VINs

When it comes to car transfers, true expertise entails examining the vehicle’s “digital soul”—the Vehicle Identification Number (VIN)—in addition to its physical state.

Interpreting the “Brand” Title

A “Clean Title” indicates that the vehicle has never been deemed a complete loss. But you need to be able to recognise “branded” titles, which have a big impact on the car’s worth and your insurance coverage:

- Salvage Title: The car was so badly damaged that the cost of repairs was more than 75–100% of its worth.

- Rebuilt/Restored Title: Originally a salvage, the vehicle has undergone repairs and passed a state inspection. Be aware that some insurance providers won’t offer complete coverage for titles that have been rebuilt.

- Lemon Law Buyback: Because of persistent, irreparable flaws, the manufacturer had to buy the car again.

- Flood/Water Damage: This brand, which is often hidden by “title washing” (moving the car to a state with laxer reporting requirements), implies that the electronics may be compromised.

The Match-Up VIN

Verify the VIN in three locations before signing the title:

- the driver’s side dashboard, which is visible through the windscreen.

- the jamb sticker on the driver’s side door.

- the actual title document. The transfer cannot legally proceed if even one character is different, and it may be a sign that the car was stolen or “clipped” (two cars welded together).

Liability and the “As-Is” Provision

The legal language used during the transfer safeguards the seller’s future from an authoritative perspective.

The Strength of “As-Is”

Almost all private sales are “As-Is,” unless you are a licenced dealer or the vehicle is still covered by the manufacturer’s bumper-to-bumper warranty. This indicates that the buyer agrees to accept the vehicle as is, including any unreported mechanical problems.

- Seller Action: Explicitly write “Vehicle sold AS-IS, with no warranties expressed or implied” on the Bill of Sale.

- Buyer Action: A Pre-Purchase Inspection (PPI) is your only defence because the sale is As-Is. The best investment you can make is to pay a mechanic $150 to $200 to examine the vehicle before you sign the title.

The Risk of “Floating Title”

When a buyer receives a signed title from the seller but never registers it in their own name—they just sell it to a third party afterwards—this is known as a “Floating Title.”

- The risk is that the original seller remains the owner in the eyes of the government. The police will visit the original seller’s home if the “floater” is involved in a hit-and-run.

- The Solution: Make sure the buyer fills out their name and address on the title in front of you, and always snap a picture of their driver’s licence.

Moving Speciality Automobiles

When you’re not working with a typical commuter vehicle, the procedure changes a little.

Modified Automobiles and Classics

The buyer must confirm that any major modifications to an automobile, such as lift kits, engine replacements, or aftermarket turbos, are permitted in their area. If the vehicle’s modified exhaust system prevents it from passing an emissions test, some states will not allow a title transfer.

Battery transfers and EVs

Software is frequently included in the “ownership” of electric vehicles (EVs). Make sure the seller “de-lists” the vehicle on their Ford, Rivian, or Tesla app. The battery lease agreement must be transferred independently of the vehicle title if the battery is leased, which is typical in some older European models.

Completing the Documentation: The DMV Visit

The official registration is the buyer’s last step. To guarantee a successful first visit to the DMV:

- Bring Original Documents: Digital scans or photocopies of titles are rarely accepted by the DMV.

- Bring a legitimate ID or a valid passport as proof of identity.

- Payment of Fees: Be ready to pay “Title Fees,” “Transfer Fees,” “Plate Fees,” and “Sales Tax.”” Depending on the value of the car, these could easily add up to hundreds or even thousands of dollars.

Frequently Asked Questions (FAQs)

1. Can I purchase or sell a car without the actual title?

Yes, in theory, but completing without one is dangerous and frequently against the law. The only official evidence of ownership is the title. Before the sale, the seller must apply to the DMV for a duplicate title if the original is lost. A notarised Bill of Sale might be adequate in certain rare instances involving vintage cars (those built before 1975), but always check with local authorities first.

2. What occurs if the car is not registered by the buyer?

For the seller, this is a significant risk. Any subsequent speeding tickets, toll infractions, or even legal liabilities from accidents may still be sent to the seller if the buyer drives off without updating the registration. The seller should always file a Notice of Transfer and Release of Liability right away following the sale in order to avoid this.

3. Who covers the sales tax and transfer fees?

The buyer is in charge of paying the DMV’s title transfer fees and sales tax in nearly all private party transactions. The seller is in charge of making sure the car’s registration is up to date on the day of sale and supplying any necessary safety or emissions certifications.

4. Can a car that still has a loan (lien) be transferred?

Until the lien is paid, you cannot lawfully transfer the title. To obtain title from the bank, the seller must repay the loan. As an alternative, the buyer and seller can meet at the lienholder’s bank to complete the payment and have the buyer receive the title directly from the bank.

5. If I have the title, is a Bill of Sale really required?

Indeed. The Bill of Sale serves as your official receipt, while the title manages the legal ownership change with the state. It records the “As-Is” status, which shields the seller from potential mechanical disputes, and the purchase price (for tax purposes).

Conclusion: Guaranteeing a Smooth Transition

Car ownership transfers are high-stakes administrative tasks that call for accuracy and openness. Both parties can successfully navigate the process and avoid common legal or financial pitfalls by following the principles of Experience and Expertise.

Success for the seller entails receiving the money safely and being released from liability. For the buyer, it means leaving with a safe car, a clear title, and the assurance that their new investment is protected by the law.

-

Uncategorized8 months ago

Uncategorized8 months agoWhat is a Good Mileage for Used Car ?

-

Uncategorized8 months ago

Uncategorized8 months agoWhy does my car shake when I brake?

-

Maintenance & Repairs7 months ago

Maintenance & Repairs7 months agoCar Radiator Repair Cost

-

Driving Tips7 months ago

Driving Tips7 months agoCatalytic Converter Transmission Cost

-

Auto News7 months ago

Auto News7 months ago3 Best Wireless Dash Cam for Car

-

Maintenance & Repairs6 months ago

Maintenance & Repairs6 months agoWhat Does an Intercooler Do?

-

Maintenance & Repairs6 months ago

Why Is My ABS Light On? 5 Common Causes, Safety Tips & Repair Costs

-

Maintenance & Repairs6 months ago

Maintenance & Repairs6 months agoHow to Inflate Tires Like a Pro: The Simple Trick to Save $500 on Gas and New Tires